Reading Time: 6 minutes

There are many factors that determine whether an organization will succeed or fail. The corporate organizational structure is a big one.

As the name suggests, the organizational structure of a corporation is the way in which its teams are structured or organized. A well-structured company is better positioned to achieve its goals (and maximize profits, if it’s a for-profit corporation).

Corporate structure varies from company to company and depends on a number of factors including the type of organization and the industry. Many organizations create and maintain a corporate org chart, which outlines the organization structure. This helps ensure roles and reporting relationships are clearly defined.

In this post, we’ll explore the basics of corporate structure, key elements of such a structure, and why corporate organizational structure matters. We’ll also share some examples of corporate organizational charts that clearly document corporate structure – and can be used as a starting point when developing yours.

What is Corporate Structure?

Before we delve into the different components of corporate structure and why such a structure matters to businesses, it’s important to first take a step back and ask ourselves, “What is corporate structure?”

In short, a corporate structure really defines how a business is run. A solid corporate organization structure outlines the function of different teams and how those teams fit together and collaborate with each other.

Why is corporate structure necessary? Corporate governance is one of the key reasons. In the past, most companies were owned and run by families. But today, this is no longer the case. Instead, there’s typically a separation between management and ownership of an organization.

Today, many organizations have created a two-tier corporate structure as a way to protect the interests of the stockholders (or stakeholders, depending on the organization). We’ll explore the components of such a hierarchy next.

Board Meeting

Ensure effective, efficient meetings with our comprehensive Board Meeting Agenda Template.

3 Components of a Typical Corporate Structure

Clearly, corporate organizational structure matters. But how is a corporation structured?

The reality is, there isn’t a one-size-fits all structure that works for all organizations. Instead, the right structure varies based on many factors, including the type of company, industry, and goals, among others. However, there are three components of corporate organizational structure that are common across most organizations: the board of directors, the management team, and the shareholders.

1. Board of Directors

The board of directors is a group of people appointed or elected to provide governance to the organization. In for-profit organizations, the board represents shareholders. In other types of organizations, the board of directors acts in the best interest of various stakeholders, which may include donors, communities, and those served by the work of a nonprofit organization.

A key responsibility of the board of directors is to hire the CEO and other leaders at the company, set their compensation, and review their performance on a regular basis. If the CEO proves to be ineffective, the board can vote on a replacement.

Other duties of the board members include:

- Strategic planning and goal setting, in collaboration with the CEO, executives, and other key stakeholders

- Monitoring financial performance

- Ensuring the organization meets all legal and compliance requirements

- Serving on committees

- Actively participating in board meetings

The members of the board are referred to as directors. Typically, a board is comprised of three types of directors:

- Board chair: This person is the leader of the board, and in some organizations, they are referred to as the board president. The board chair is responsible for ensuring the board runs smoothly and achieves its goals. The chair works closely with company leadership to develop strategic plans.

- Inside directors: Inside directors can be shareholders or top managers within the company. These folks are responsible for high-level budget approval, implementing and overseeing strategy, and approving major projects and initiatives. Because they are from inside the organization, they are able to share a unique, internal perspective with other directors.

- Outside director: As the name suggests, outside directors are from outside of the company. While their duties are similar to inside directors, they’re not directly part of the company management team. Outside directors offer unbiased perspectives on issues that come to the board.

At some organizations, the board is outlined in a board of directors organizational chart. Such a chart may also include information about the directors’ experience, as well as information about their terms. This can be an important tool for recruiting purposes, as well as succession planning.

2. Corporate Officers

Corporate officers are the second component of an organization’s structure. Corporate officers, also referred to as the management team, are chosen by the board of directors and are directly responsible for the company’s day-to-day operations.

The management team typically includes the CEO, Chief Financial Officer (CFO), and Chief Operations Officer (COO).

- CEO: The CEO is the top manager at the organization and is responsible for the organization’s entire operations. This person reports to the chair and the board of directors and is responsible for carrying out board decisions and initiatives. In collaboration with senior management, the CEO ensures the organization is running smoothly. Sometimes, the CEO also serves as the president.

- CFO: The CFO reports to the CEO and oversees the organization’s finances. Typical duties include preparing budgets, analyzing financial data, monitoring costs and expenditures, and reporting on financial performance.

- COO: The Chief Operations Officer oversees the operations of the organization; however, they are typically more hands-on than the CEO. COOs are in charge of areas including marketing, sales, production, and human resources.

Shareholders

Shareholders are those who own a part (or shares) of a publicly traded company. They are also commonly called stockholders. Shareholders can be individuals, companies, or institutions, and the number of shareholders is based on the business entity structure. For example, the maximum number of shareholders an S Corporation can have is 100. However, a C Corporation can have an unlimited number of shareholders.

Typically, shareholders aren’t personally liable for the company. However, they do have the ability to vote on certain issues, such as:

- Changes to the articles of incorporation or bylaws

- Whether the company merges with another

- Who serves on the board of directors

- How to dispose of assets

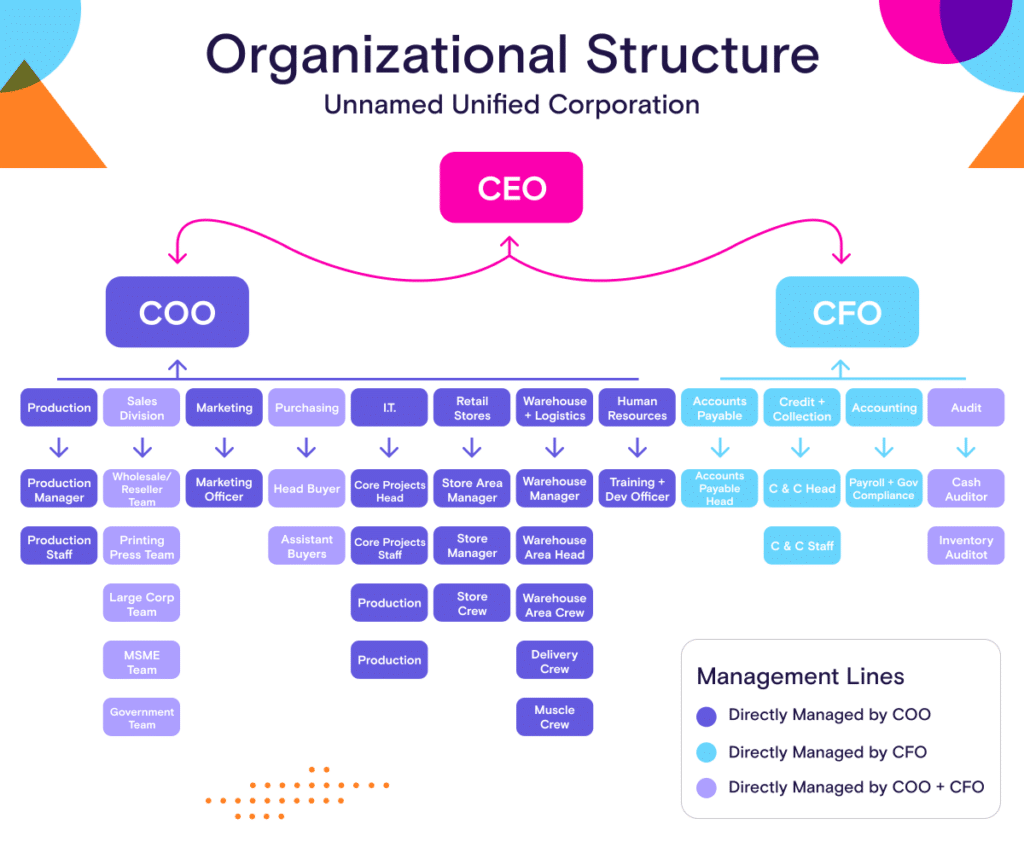

Corporate Structure Chart Example

An corporate organization chart – often referred to as a corporate org chart – is a diagram that illustrates how an organization is structured. It includes the different components of the organization’s structure, as well as how these components are related to each other.

It’s important to develop a corporate org chart, which can include the board of directors org chart. Doing so ensures everyone is on the same page as far as structure, collaboration, and reporting.

It can be overwhelming to develop an org chart from scratch. Of course, all organizations are different. However, a great starting place is to look at well-developed corporate org charts (see example below) and board of director org charts.

Why Is Corporate Structure Important?

While there was once a time when company owners and managers were one and the same, this has become a lot less common. Corporate organizational structure is key to effective governance, as it clearly separates owners and managers of the company.

In addition, when positions in a corporate structure are documented, it helps ensure the operations of the entire organization run smoothly. Companies are better positioned to achieve their goals, grow, and attract new investors.

Let’s zero in on a few of the key reasons why corporate organizational structure (and an org chart) is so important.

- More effective communication: Clear communication is essential to the operations of any business. Conversely, miscommunication can lead to some big problems. An organization structure helps ensure everyone throughout the organization understands with whom they need to share different information.

- Clear reporting relationships: An effective corporate structure outlines how different teams and individuals are connected to each other. Everyone knows whom they are responsible for – and whom they are accountable to. This eliminates the confusion of who is responsible for what.

- Goal achievement and growth: Corporate structure ensures tasks can be completed more efficiently. Everyone understands their roles and responsibilities – and how this fits in with the overall structure of the organization. This helps the company achieve its goals and mission and continue to grow.

Have You Defined Your Corporate Organizational Structure?

A company’s organizational structure lays the foundation for how to run the entire business. With a solid organizational structure, organizations are better positioned to achieve their goals and grow.

It’s essential to develop an organizational structure that works for your business – and then document it using an organizational chart. A great place to start is by finding good examples of existing org charts – and then modifying them to fit the needs of your organization.

In addition, a board portal like OnBoard can help you manage the roles and terms of your board members, which can improve your recruiting and succession planning efforts. With OnBoard, you can track your board’s experience, background, and term limits – all in one central location.

In fact, OnBoard can help you simplify all aspects of board management and ensure your directors have all of the documents, information, and communications they need to achieve more for your organization – all within a single platform.

Ready to learn more? Start your free trial of OnBoard today.

Product Overview

Enhance strategic meetings with OnBoard's intuitive board management tools.

Board management software helps keep meetings on focus and board members happy. Download our Board Management Software Buyer’s Guide to learn more.

About The Author

- Adam Wire

- Adam Wire is a Content Marketing Manager at OnBoard who joined the company in 2021. A Ball State University graduate, Adam worked in various content marketing roles at Angi, USA Football, and Adult & Child Health following a 12-year career in newspapers. His favorite part of the job is problem-solving and helping teammates achieve their goals. He lives in Indianapolis with his wife and two dogs. He’s an avid sports fan and foodie who also enjoys lawn and yard work and running.

Latest entries

Board Management SoftwareMarch 24, 2026AI Oversight for Board of Directors: Risks, Benefits, and Best Practices

Board Management SoftwareMarch 24, 2026AI Oversight for Board of Directors: Risks, Benefits, and Best Practices Board Management SoftwareJanuary 8, 2026Corporate Board News, January 2026: Shifting Legal Protections, Jurisdictions

Board Management SoftwareJanuary 8, 2026Corporate Board News, January 2026: Shifting Legal Protections, Jurisdictions Board Management SoftwareJanuary 8, 2026Nonprofit Board News, January 2026: Responding to Rapid Change

Board Management SoftwareJanuary 8, 2026Nonprofit Board News, January 2026: Responding to Rapid Change Board Management SoftwareJanuary 1, 2026AI Meeting Minutes Generator: 5 Best Options in 2026

Board Management SoftwareJanuary 1, 2026AI Meeting Minutes Generator: 5 Best Options in 2026